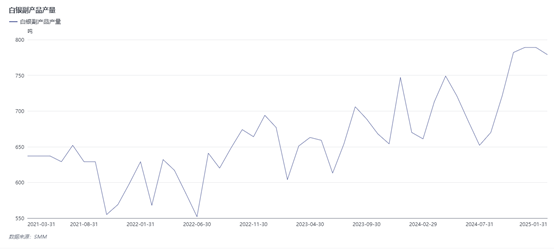

According to SMM, the production of silver by-products from primary lead smelters is expected to steadily increase in 2024, with a cumulative total exceeding 8,000 mt, up over 7% YoY.

The increase in silver production from lead smelters in 2024 will mainly occur in H2. On one hand, the tight supply of lead concentrates and silver-lead ores in H1 2024 limited the production of refined lead and precious metal recovery at several lead smelters. This raw material shortage is expected to ease with the recovery of overseas supply and the concentrated arrival of imported ores at smelters. Additionally, silver prices in 2024 are operating at a near five-year high, prompting lead smelters to prioritize higher recovery rates of precious metals by using raw materials with higher silver content, thereby achieving greater "coefficient difference" profits.

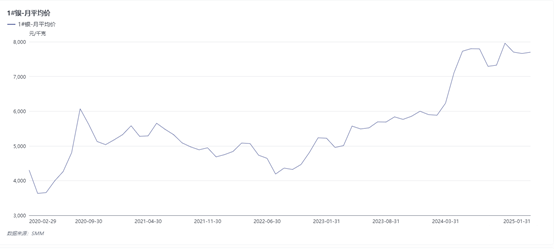

In the raw material market, due to the rangebound movement of silver prices from 2020 to 2023, the pricing coefficient for silver in lead concentrates (with silver content of 200–2,500 g/mt) was frequently adjusted. For certain mine products with silver content below 1,000 g, the pricing coefficient was adjusted only 1–2 times annually. Since 2024, with silver prices surpassing 6,000 yuan/kg, the pricing coefficients for silver in various types of lead ores have been raised. At the beginning of 2025, under a macro environment of heightened risk-aversion sentiment, the precious metals market is expected to remain bullish, and lead smelters continue to hold optimistic expectations for silver prices. In certain regions, the pricing coefficient for silver-lead ores with silver content of 1,500–2,500 g/mt has shown signs of slight increases again. However, smelters are not optimistic about the silver-rich content of newly constructed lead-zinc projects. Despite the high added-value attribute of silver remaining a major source of revenue for lead smelters in 2025, the supply of silver-bearing lead ore raw materials is still in undersupply, and the growth rate of silver production from lead smelters in 2025 may slow down.